Time series Modelling and analysis

Advanced Modeling and Control

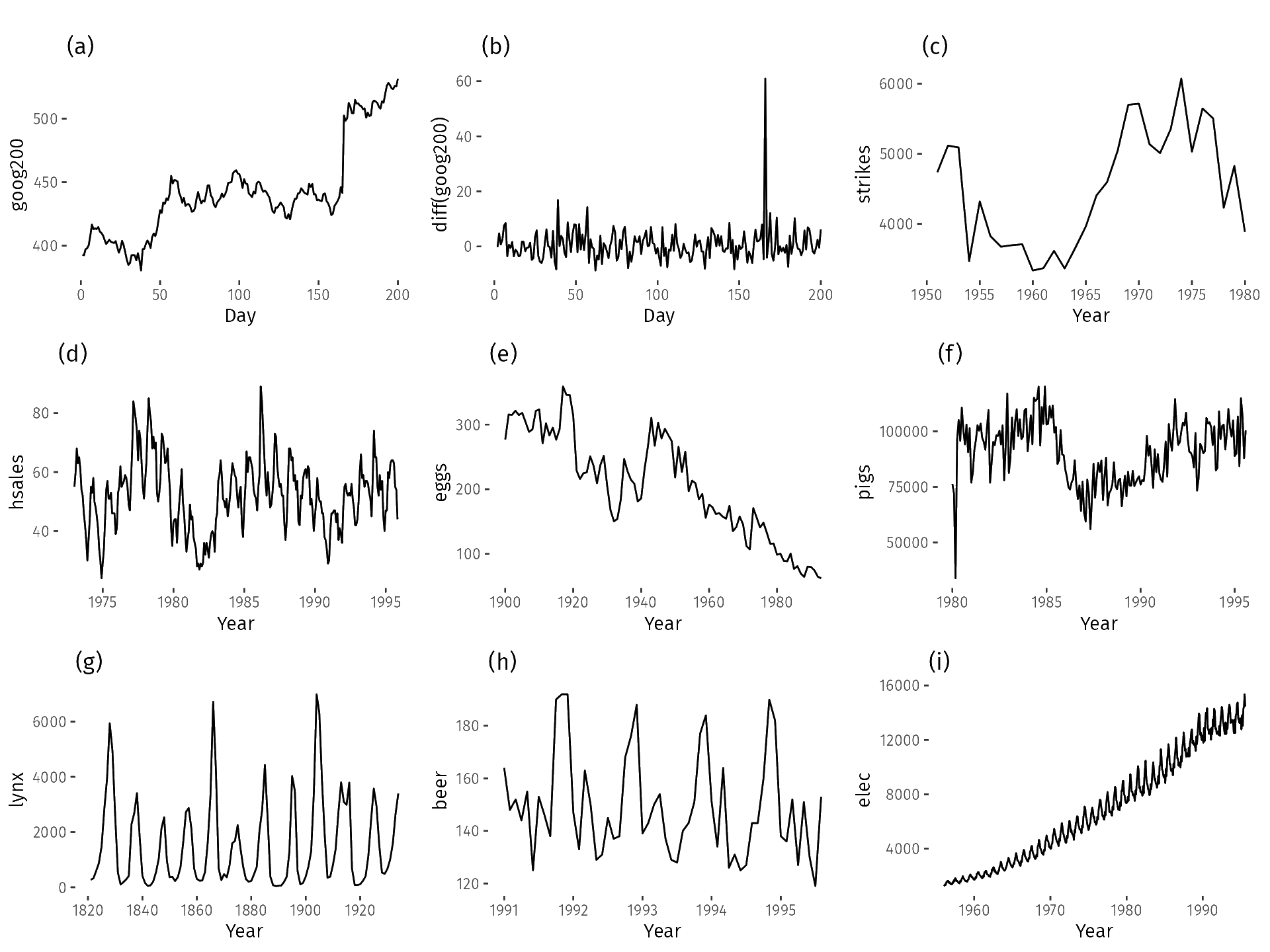

What is Time Series?

- A time series is a sequence of observations recorded at successive points in time

- Each observation is ordered, meaning the position in time matters

- Data is often collected at regular intervals:

- Seconds, minutes, hours (process monitoring sensors)

- Days, months, years (economic, environmental, health data)

- Seconds, minutes, hours (process monitoring sensors)

Stationary vs Non-stationary

Stationary series

- Mean and variance constant over time

- Fluctuates around a stable level

- Easier to model and forecast

Non-stationary series

- Mean or variance changes with time

- Shows trend, seasonality, or shifts

- Requires differencing or detrending

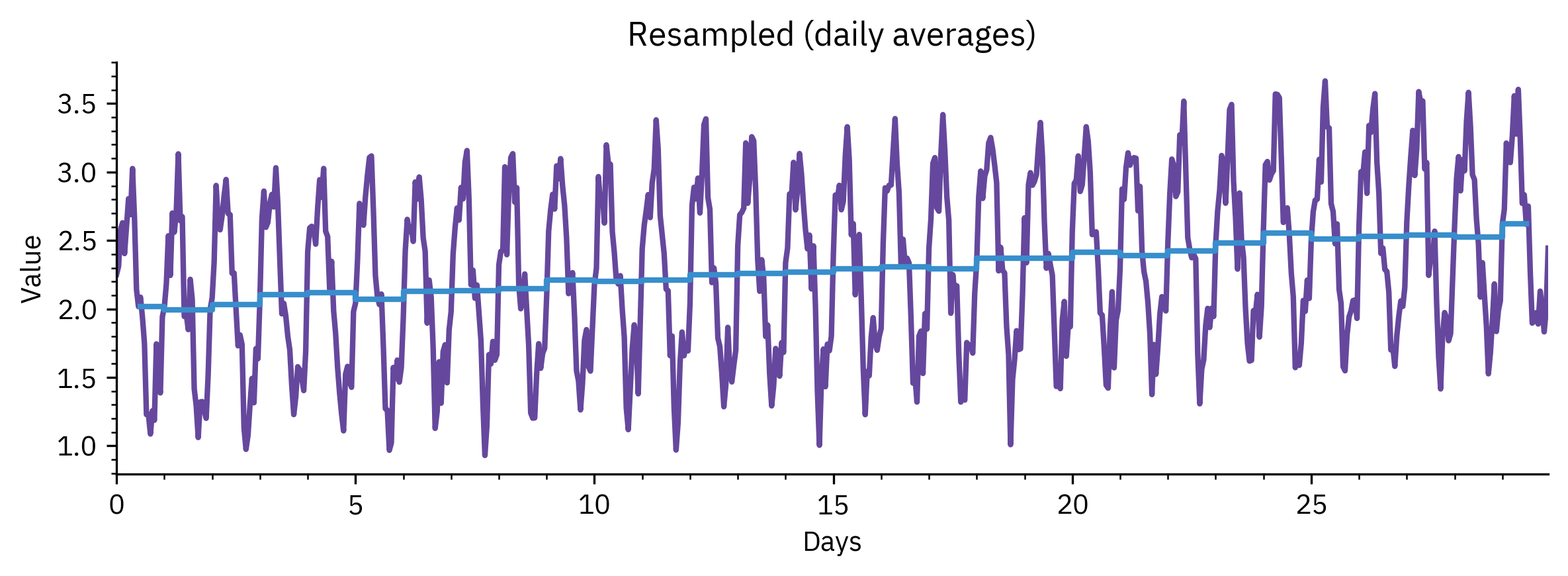

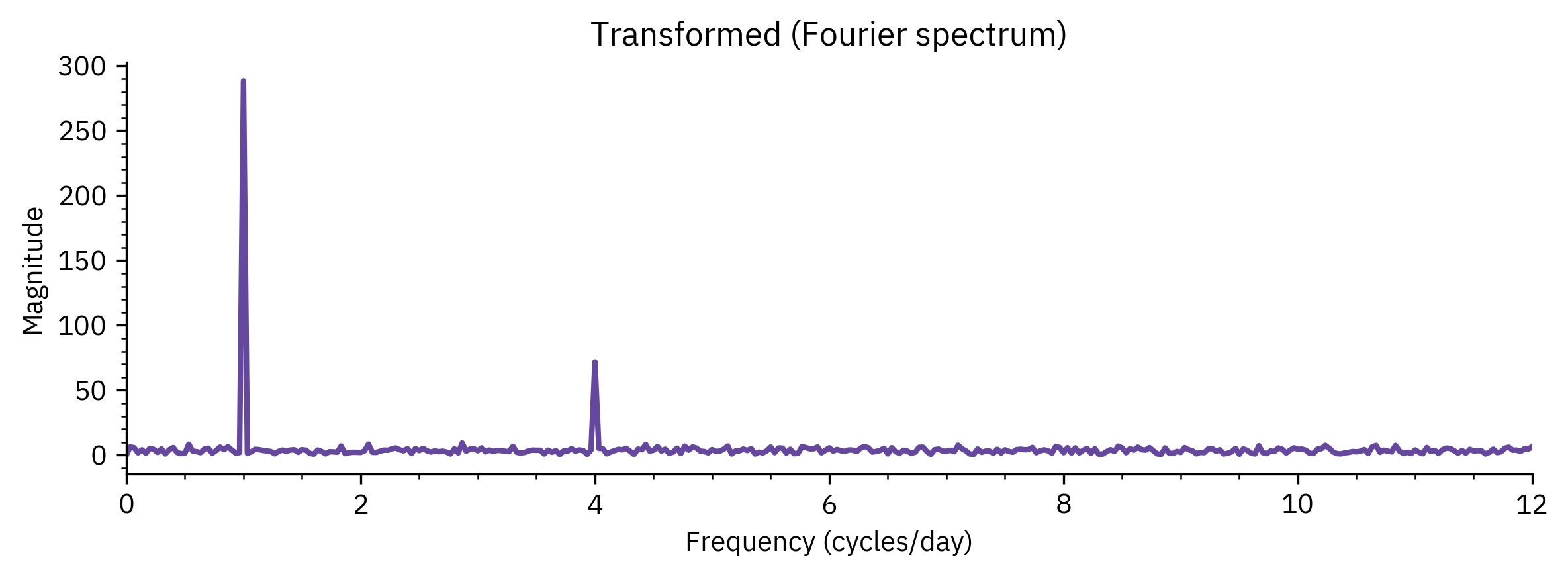

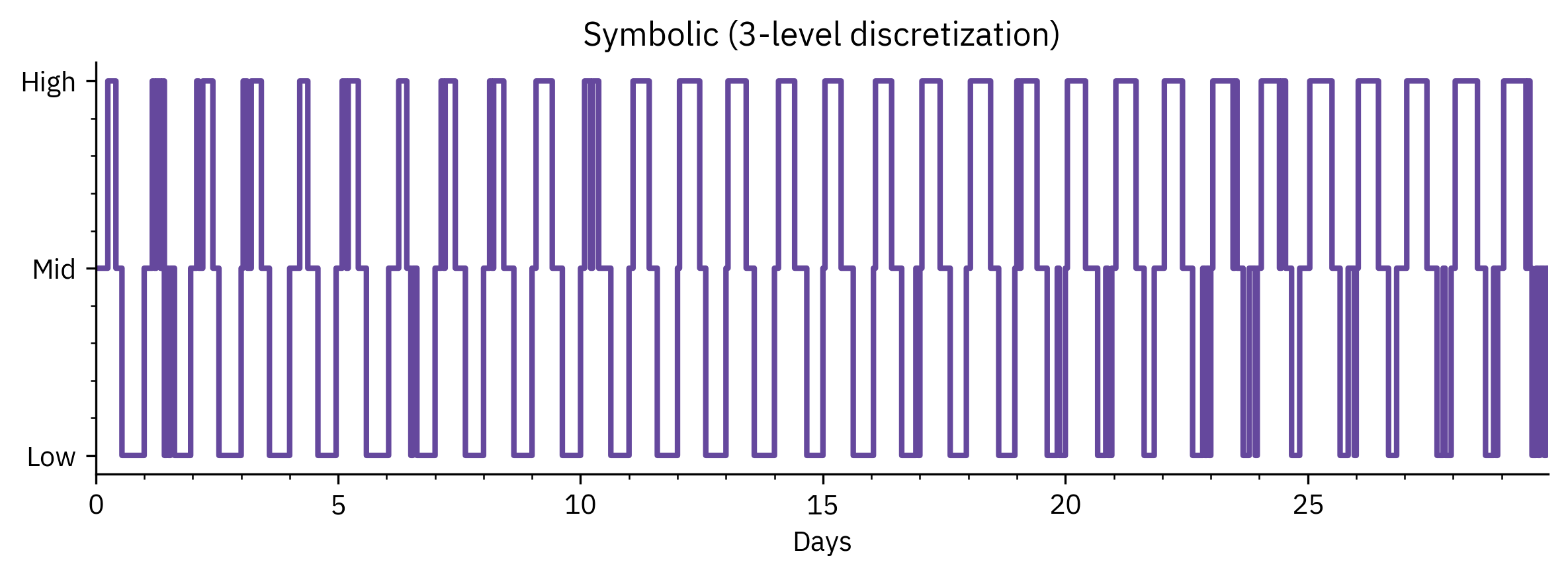

Time Series Representation

- Time series often large and high-dimensional

- Representation helps simplify analysis and comparison

- Common approaches:

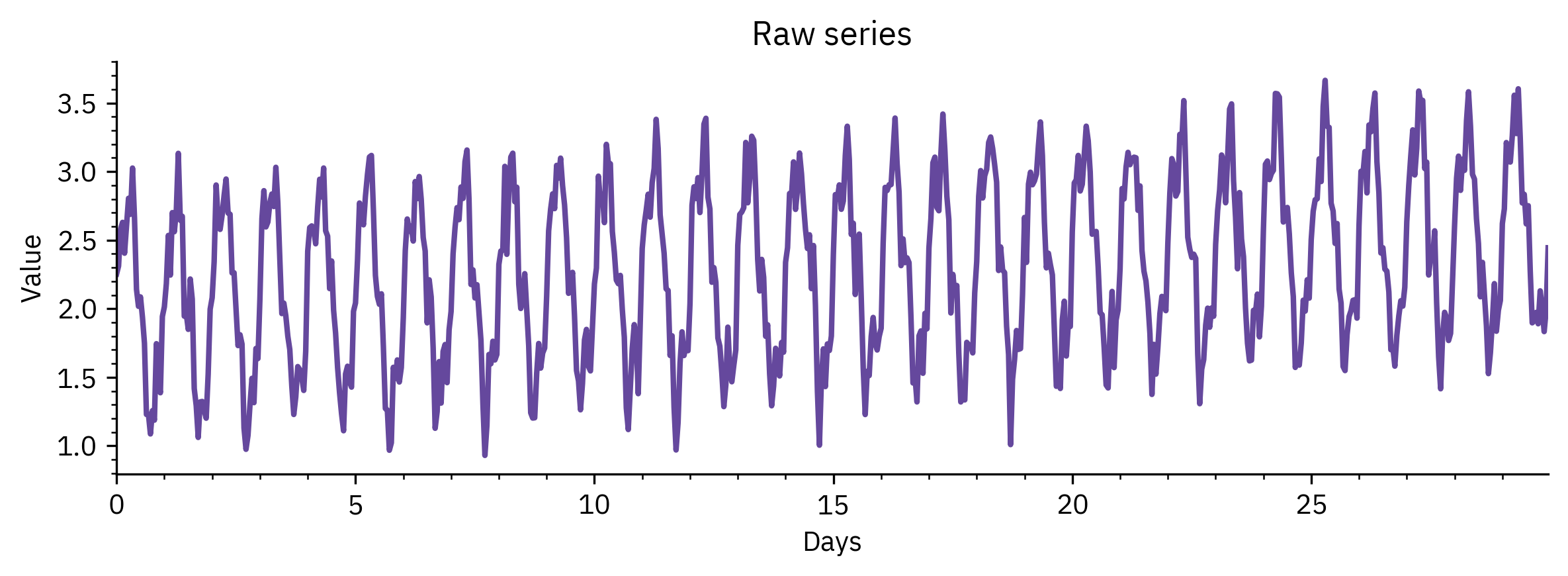

- Raw series (original data)

- Resampling (reducing data points, e.g., daily → monthly)

- Transformation (Fourier, wavelets, PCA)

- Symbolic representation (grouping values into categories)

- Raw series (original data)

Benefits

- Reduces dimensionality while preserving essential patterns

- Enables efficient similarity search and clustering

- Provides basis for further tasks:

- Pattern discovery, Classification, Forecasting

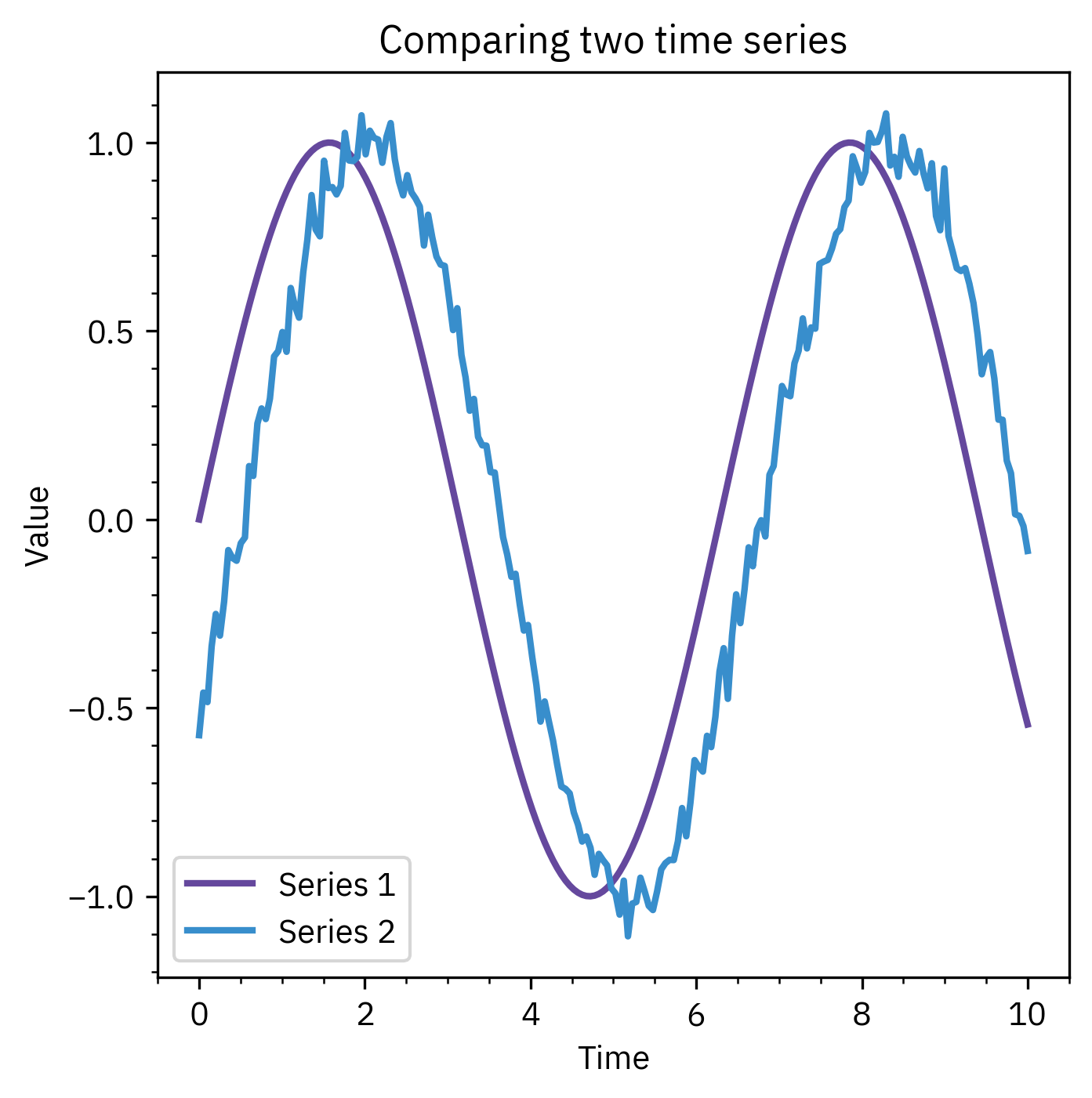

Similarity Measures

- Used to compare two or more time series

- Important for:

- Clustering and classification

- Pattern discovery

- Anomaly detection

- Common measures:

- Euclidean distance

- Correlation-based distance

- Dynamic Time Warping (DTW) for misaligned series

- Euclidean distance

- Euclidean distance works if sequences are aligned

- DTW allows matching when sequences are stretched or shifted

- Correlation-based measures capture shape similarity

- Choice of similarity measure affects clustering, anomaly detection, and forecasting

Characteristics of Time Series

- Temporal dependence: current values often depend on past values

- Directionality: useful for forecasting forward in time

- Patterns may include:

- Trend (long-term increase or decrease)

- Seasonality (repeated cycles, e.g., daily, monthly, yearly)

- Random fluctuations (noise)

- Trend (long-term increase or decrease)

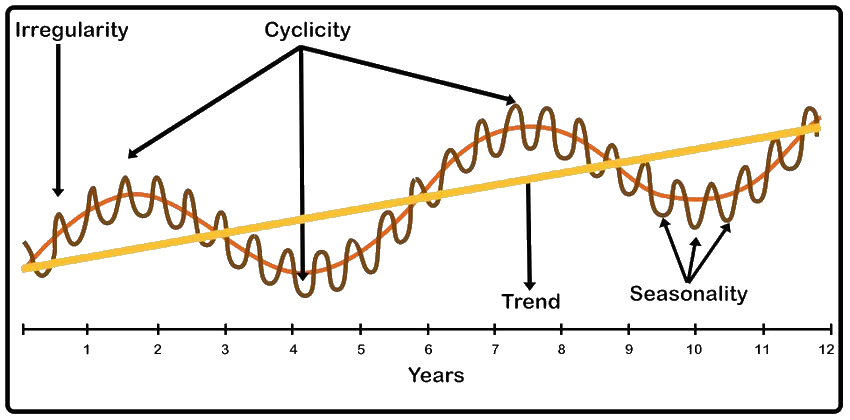

Time-Series Decomposition

- A time series can be expressed as the sum of underlying components

- Trend: long-term direction

- Seasonality: repeating cycles

- Cyclic variation: slower, irregular fluctuations

- Residual: noise or unexpected shocks

- Trend: long-term direction

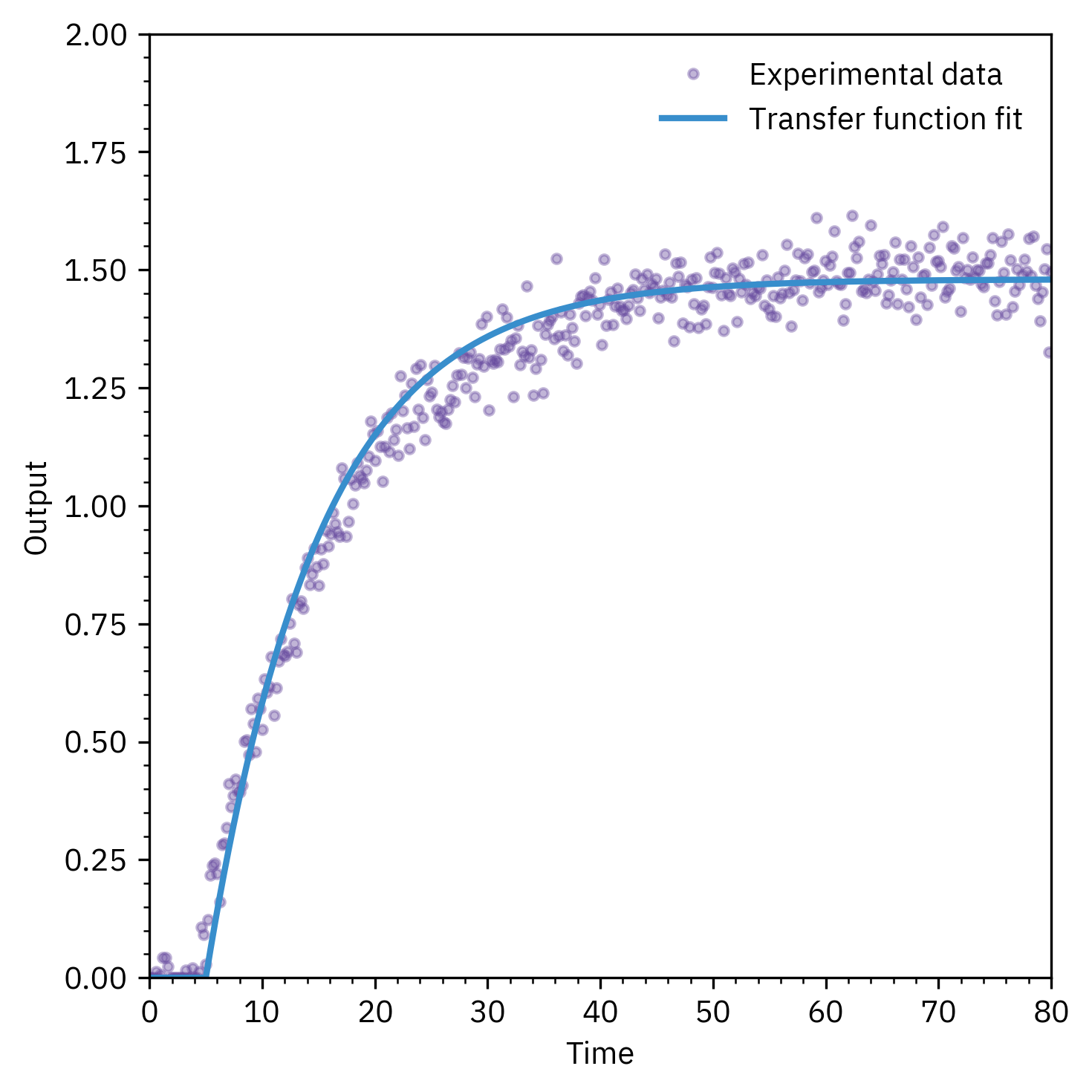

Transfer Function Models

- Many physical processes can be represented by transfer functions in the Laplace domain

- Transfer function relates input → output dynamics

- Useful for:

- Capturing process gain, time constant, and delay

- Providing a baseline for time-series model comparison

- Often estimated from input–output data (system identification)

Transfer Functions as a Starting Point

- Physics-based intuition: order, delay, stability

- Provides initial guess for data-driven models (ARX, ARMAX)

- Bridges between first-principles modeling and time-series modeling

Autoregressive (AR) Models

- Concept

- Current value depends on a linear combination of past values

- AR(p):

y_t = \phi_1 y_{t-1} + \phi_2 y_{t-2} + \dots + \phi_p y_{t-p} + e_t - Captures short-term correlations in stationary data

- Current value depends on a linear combination of past values

- MATLAB

ar(data, order)estimates AR model

- Order selection via AIC / FPE

- Applications

- Forecasting short horizon

- Identifying dominant lags

- Noise modeling in ARMAX

- Forecasting short horizon

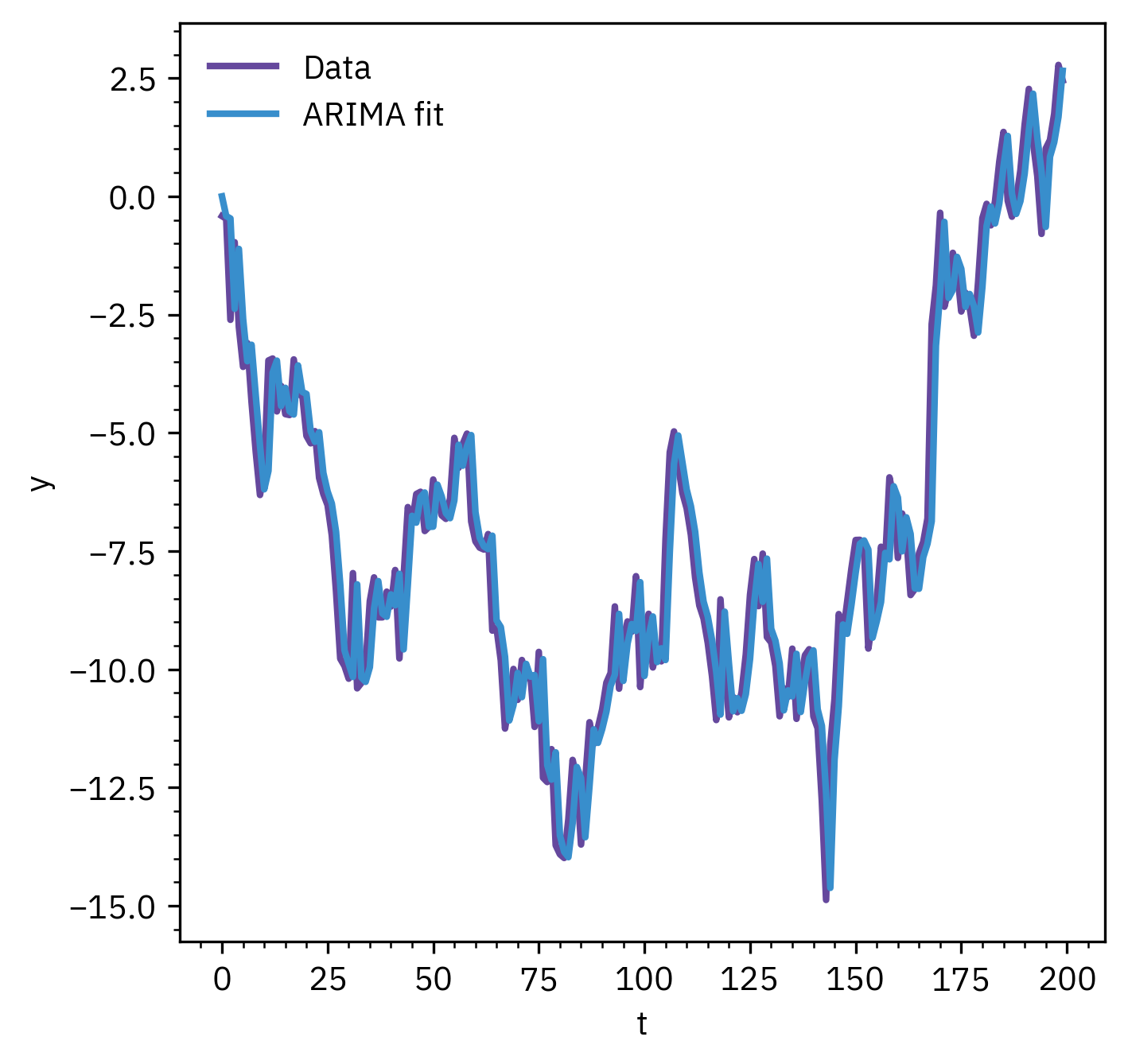

ARIMA Models

- ARIMA = Autoregressive Integrated Moving Average

- Extends ARMA for non-stationary series

Integration differencing step

\nabla y(t) = y(t) - y(t-1)

Makes the series stationary before ARMA modeling

- Interpretation

- AR: memory of past values

- I: removes trends and seasonality

- MA: corrects random shocks

- AR: memory of past values

MATLAB

m = arima(p,d,q)

p = AR order; d = number of differences (integration order); q = order of MA part